Savings

Happy New Year to everyone! I hope 2022 brings you everything you want including but not limited to more Bitcoin! Taking advantage of this prolonged dip in the price is a blessing in disguise and a great way to grow your share in the network. Currently one dollar buys you ~2,400 satoshis, the smallest unit of a Bitcoin. I’m buying every single payday without hesitation.

Using Bitcoin as a long term savings account is a wonderful tool but what should you do with the rest of your savings? The savings you don’t want to put at risk. The savings that you have around for an emergency or peace of mind.

The importance/value of saving has been lost through years of manipulating the money supply and it is very unfortunate to see. Your dollar is worth less tomorrow than it is today so everyone is incentivized to spend or invest. This is why corporations and people alike DO NOT having money around for a raining day or an economic downturn. Wether it is a conscious or subconscious thought, saving money is completely disincentivized. A society without savings is a society dependent on government and the bailouts they can provide which in turn makes things even worse.

If you hold your savings under your mattress or in a traditional savings account you are losing purchasing power every single day as prices are rising. It goes unnoticed throughout the days but it is very evident throughout the years. You must earn interest on your savings or you are falling behind. It’s that simple. My goal would be to at least match the rate at which money is being printed. We can see this rate by looking at the year over year change in M2 money supply via ycharts.com which currently sits at 13.07%! 2020 and 2021 we were over 20%. Good luck keeping up with numbers like that let alone planning for a retirement.

So back to our original question, what do you do with your personal savings account? Leave it in cash/traditional savings account and fall behind? Invest it and expose yourself to a lot of risk? Plus waste your time looking for where to invest it. Not everyone is a professional investor even though it seems like it these days.

STOP! I just wrote this article with the plan of directing you towards earning 8-9% on your savings. I have used this strategy extensively but it has been several months since adding to it and I don’t think it is going to work anymore. Long story short, within this ecosystem we have Bitcoin and we have everything else. Bitcoin at its base layer is slow and methodical. Bitcoin only does ~7 transactions per second and then the scaling to millions of transactions is happening on top of Bitcoin in layer two and three applications. You can read more about this is my previous writing on layered money, TRH #12.

The strategy I laid out below (scroll down to see) uses coins pegged to the dollar known as “stable coins” which allow you to be in the “crypto” ecosystem while avoiding the volatility. They are very popular. You can deposit these stable coins with companies and earn attractive interest rates. Unfortunately all of this stuff is built on top of ethereum and the ethereum network thinks it can do all it’s scaling of transactions on its base layer. This is resulting in a TON of congestion and has a very expensive cost per transaction. Look below at me trying to send $50….. $31 of it goes to fees. I have savings in this stuff and am currently wondering how to proceed. I want to be clear, this is not at all a problem with Bitcoin. It is a problem with everything else and a glaringly obvious example that none of this other stuff is even a close second to Bitcoin. Unfortunately at this time I cannot recommend anything besides saving in the traditional sense and long term savings into Bitcoin. I left the rest of the newsletter below in case you are interested in the process.

I keep my savings with a company called Blockfi because I am able to earn 8-9% interest while I simply save. No investing, just saving. This is helping me and countless others attempt to keep up with the rate that money is being printed. They can offer these rates because they are a digital company with a lot less overhead costs like buildings, maintenance, and employees. They provide lending services which also assists in providing these rates. You can earn interest on several different coins but I personally just use it for dollars and do not recommend it with your Bitcoin as you are now trusting a 3rd party. Any interest earned over $500 I believe is counted as taxable income and they provide you with an end of year form.

You can see all their rates here.

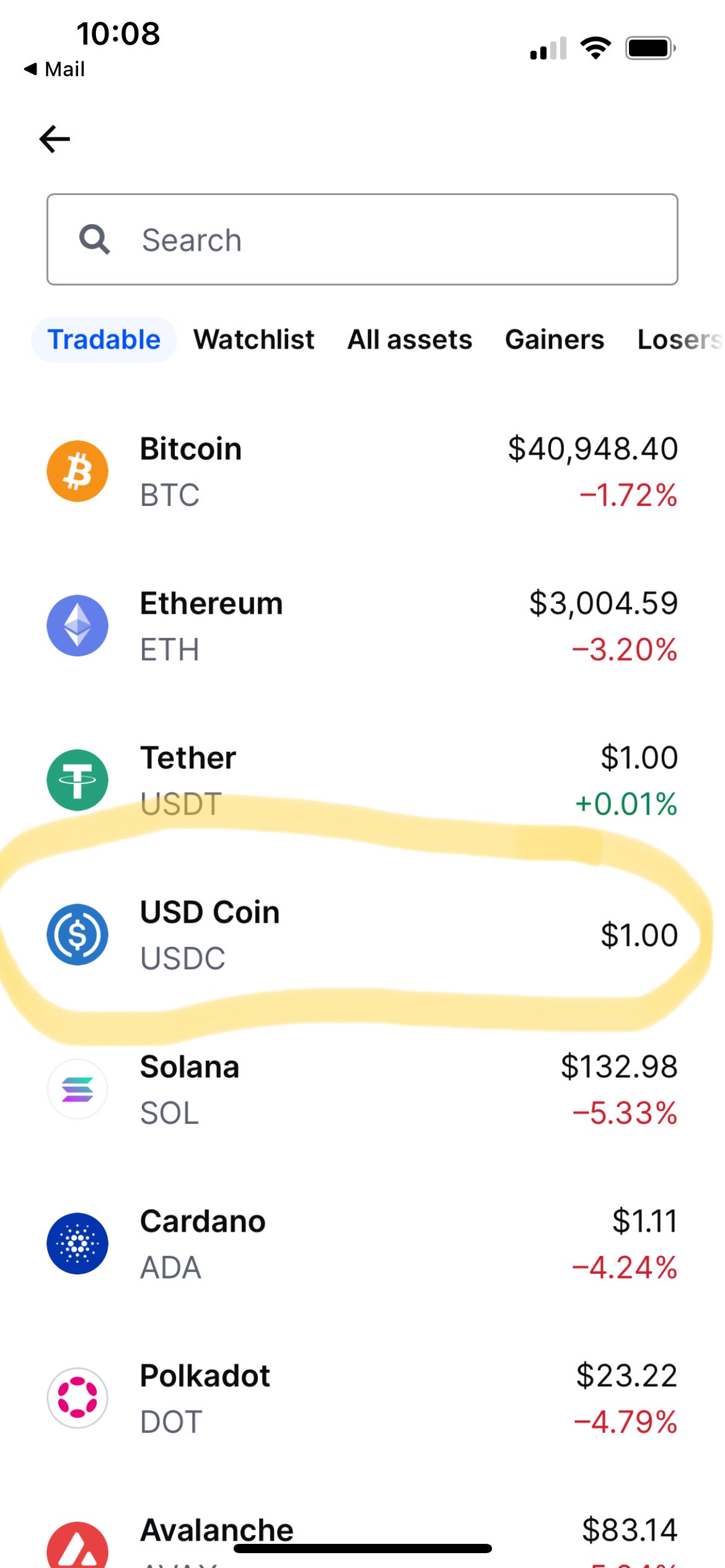

How do you get dollars onto blockfi? This is where the friction exists, getting your analog dollars into digital form otherwise known as stable coins. They are pegged 1:1 to the dollar. Examples of this are coins with “USD” in the name like USDC, GUSD, BUSD and many more. I hope this isn’t confusing anyone but it probably is, for that reason I will walk you through an example on coinbase with USDC - one of the largest stable coins.

Login to your account and try to ignore all the shitcoins. You can search “USDC” or find it, it should be near the top. Notice how its value is $1

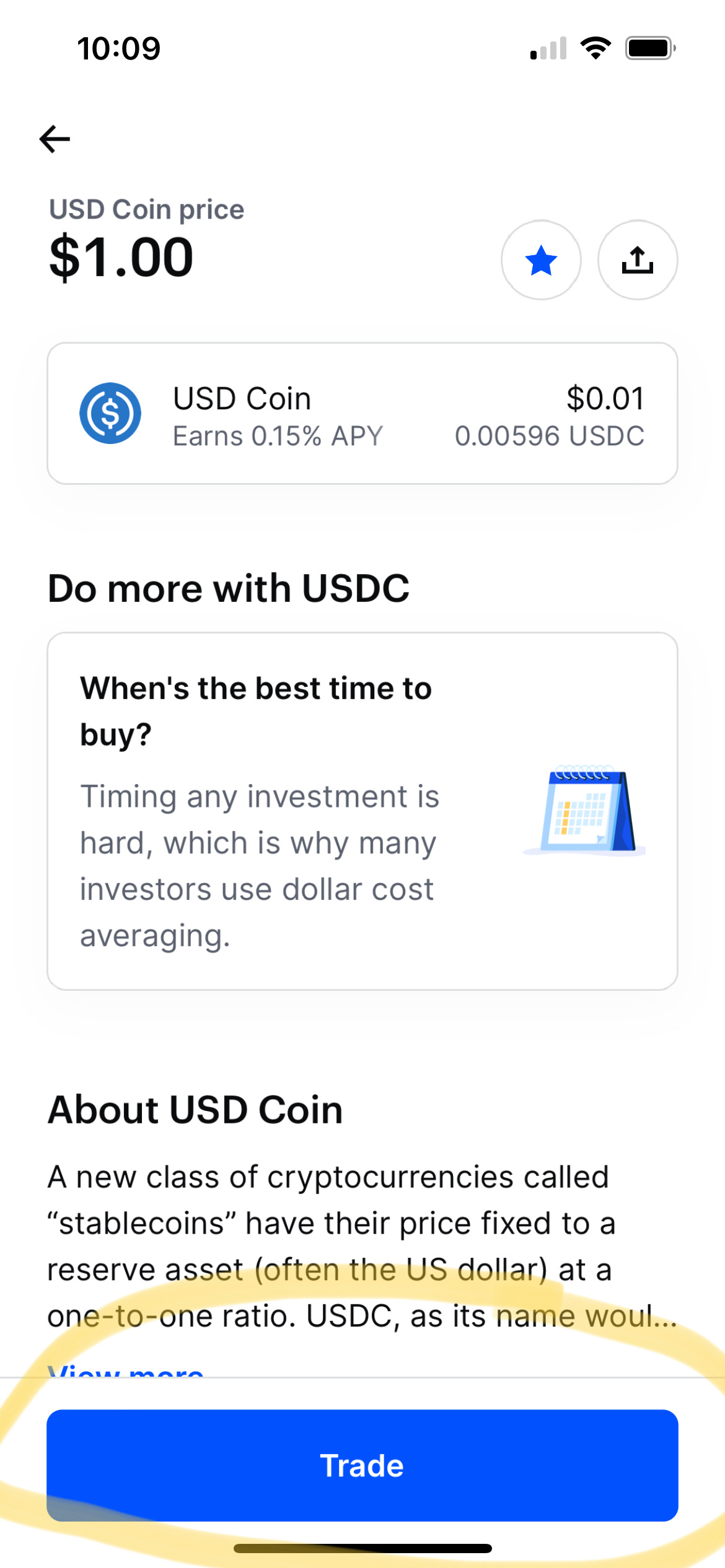

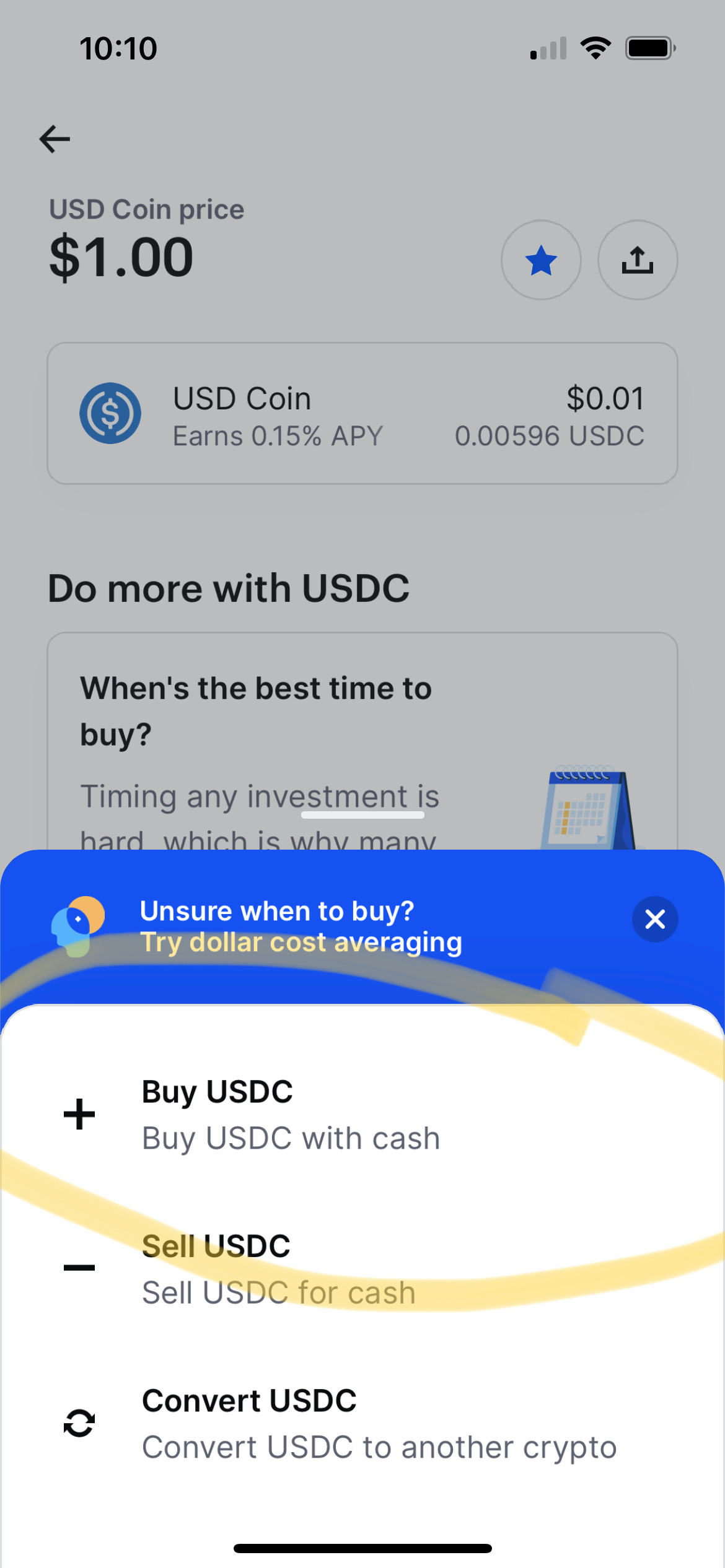

You can then read a bit about it and eventually click on “trade.”

You simply buy USDC, in any amount you’d like. It’s value remains pegged to the dollar and you are now in the “crypto” ecosystem and not exposed to all the volatility.

Next step is sending your money to blockfi to earn your interest. Create an account and find USDC. Click on “fund” and this will provide you with an address with which to send your funds from coinbase to blockfi.

Ok that was a bit much for me but something to reread a few times! Thanks Mr Rabbit!