Cantillon Effect

How do they “print” new money? Is it evenly distributed amongst every person or does it fall into the hands of the few? How does that money effect society? These are a couple questions I would like to answer and elaborate on.

New Money

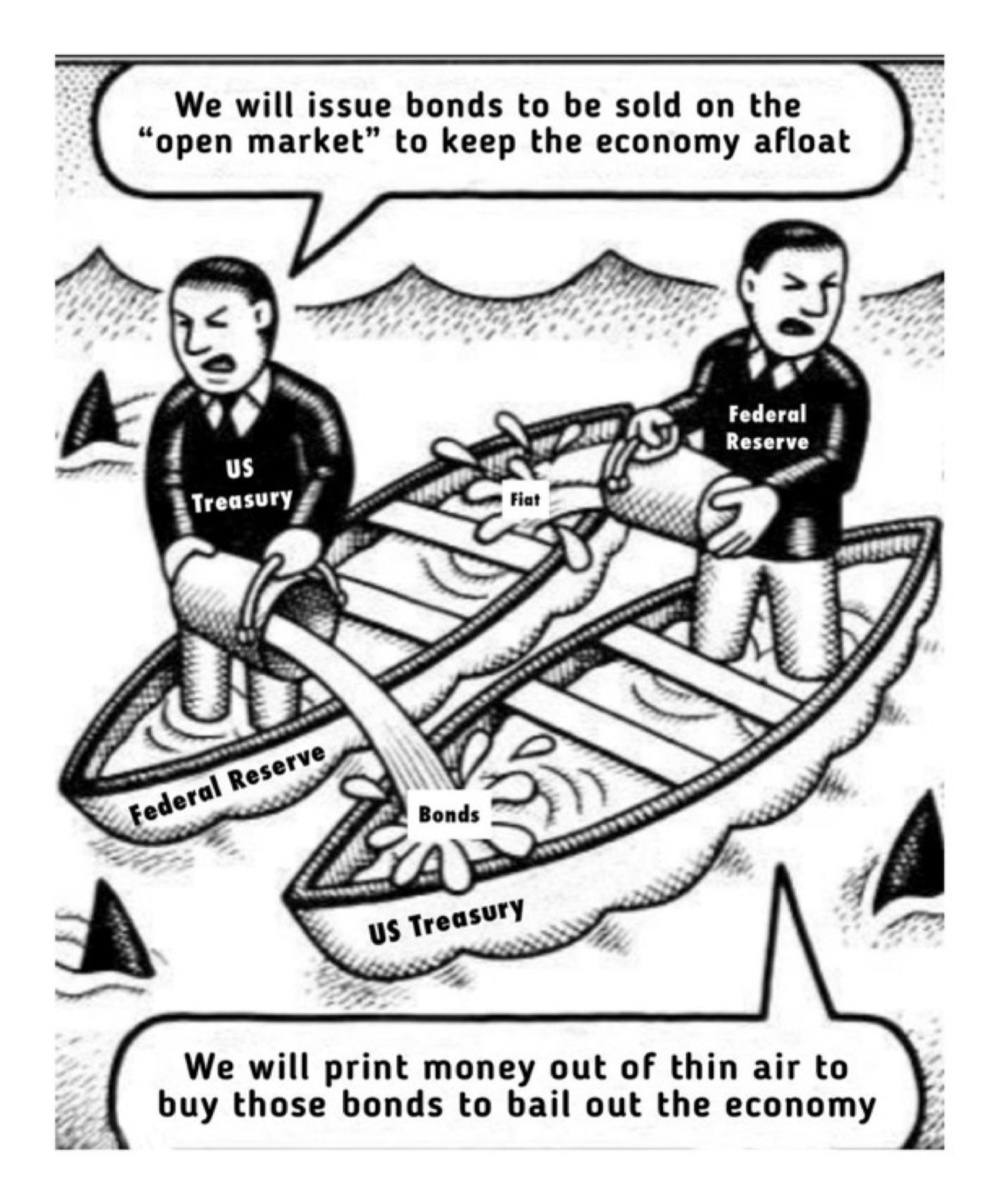

First and foremost we should explain how new money enters the system. It is not just dropped down from a helicopter for everyone to grab. One way that new money is created is that the US Treasury creates bonds which is then “bought” by the Federal Reserve (an unelected private corporation). These bonds are bought with that newly created money. In other words, the printing of money is done through financing debt because a bond is just a debt contract or said another way, an IOU + interest.

What the hell Nick, this is confusing! So you’re telling me that a bond is debt + interest and you’re also telling me that the printing of money is just purchasing newly creating bonds. Then the printing of money is just buying debt? Yes. This process is called monetizing the debt. After the 2008 financial crisis the concern was as follows:

The Federal Reserve System of the United States creates the country's monetary base. Since August 2008, the Fed has tripled the monetary base from about $0.8 trillion to $2.7 trillion. More than half of this new money was used to purchase U.S. government bonds (Treasury debt), which has led some commentators to complain that the Fed is "monetizing government debt." The concern is that the Fed's actions are somehow enabling excessive government borrowing and possibly risking future inflation.

Do we have excessive government borrowing? Yes. Do we have inflation? Yes. Are we surprised? No. This was written in 2013!! That monetary base they are describing is currently about to pass $9 trillion. Click here for the full article.

The other way money is being “printed” is through the Federal Reserve purchasing mortgage backed securities (MBS). You probably just asked yourself, wtf is a MBS?? Let’s break it down - a security is a fancy word for a financial instrument like a stock or bond. These securities are backed by real life mortgages hence the name, mortgage backed security. Just like Apple stock is backed by the company and profits of Apple but we don’t call it Apple backed security we just call it Apple. Instead of mortgage backed security, we could just call it mortgages. The Federal Reserve is again issuing debt (new money) and buying mortgages. Who the heck owns all the mortgages? Funny you ask. The government, via programs like Fannie Mae and Freddie Mac. They don’t own the actual house, unless you default on your loan, but rather they own the financing of the loan. According to Bankrate.com 62% of mortgages are owned by these government programs.

Neither Fannie Mae nor Freddie Mac directly provide mortgages to homebuyers. Instead, you’ll get your loan from a mortgage lender, such as a bank, credit union or online lender, which can then choose to sell the loan to one of these GSEs, assuming the loan’s eligible. As of 2020, Fannie Mae and Freddie Mac owned 62 percent of conforming loans.

Wow, this is a lot to take it. Let’s try to simplify this. You get a mortgage from your local bank, they sell it to the government, then the government sells it to the Federal Reserve for new dollars that didn’t exist before. This again is called monetizing the debt. The sale of old debt for new debt. Yikes! Sounds like an absolute house of cards, no pun intended.

Who Benefits

Those with access to the financial markets as well as those who own a house/real estate. Ask yourself two simple questions. Why is Wall Street thriving? Why is the cost of a house skyrocketing? I would say it has something to do with all this new money creation and the way it is created. This hurts individuals who don’t have access to the market and who don’t own a house which in turn further divides this country via wealth inequality. The rich get richer and the poor get poorer. The individuals closest to the money spigot benefit while the people further away suffer. This is called The Cantillon Effect.

Here is a snippet from mises.org explaining the effects of “new money.”

It is shown here that there are winners and losers from new money. For example, the Fed’s monetary expansions tend to help the wealthy, banks, big corporations, and the financial industry more generally. Subsequently, as prices rise, the Fed’s policy hurts retirees, those on fixed incomes, and wage earners who receive the new money last, if at all. This is one reason why the Fed and most mainstream macroeconomists vigorously deny the existence and importance of Cantillon effects and adopt the assumption of neutral money. Tragically, they often get away with this ruse because the theft cannot be directly seen, except in the final result.

Bitcoin Fixes This

Bitcoin has a fixed money supply. It is immune to human corruption. This prevents us from “printing” new monetary units and manipulating the system with which society operates. Bitcoin offers a fair money that works. It is that simple. If you want more money you need to provide a net benefit to society. Bitcoin operates on a proof of work system, not a proof of being closest to the money spigot. Bitcoin enables true free market capitalism. No bailouts. No handouts.

Closing Thoughts

The next question you should be asking yourself is, who is going to pay back all of this debt? The answer is always - our future generations. The proverbial “kicking the can down the road.”

Taking on debt is saying we want something now that we can pay for later. Debt is literally pulling productivity forward at the expensive of future generations. At what point are we going to accept that we ARE that generation that is paying for it. Forget the next generation, this world sucks right now! The next generation doesn’t stand a chance as long as this debt riddled fiat monetary experiment exists. Bitcoin offers a solution.

I’ll leave you with a question to ponder.

If the government is creating new money and buying all the mortgages, thus sending housing prices through the roof (pun intended this time), do we think house prices go up for as long as they print? Is it a bubble or is it the beginning of a hyperinflationary event? I’ll take the latter.